Tidewater Inc. ($TDW) - A Deep Value O&G Investment Opportunity

Over the past couple of years, I’ve been particularly fixated on the energy sector. What first started as an investment muse in 2020 became a new mental framework that has greatly enhanced my understanding of the world and financial markets.

The underlying conclusion that I’ve developed is that we’re currently living in an increasingly energy constrained world. After years of rapid production (2000-2014), followed by years of oversupply and underinvestment (2014-2022), the world is now likely entering a period of prolonged energy shortages, especially one in oil and gas.

In a previous post, I provided a high-level overview for why oil and gas is critical to life as we know it. I was encouraged to find that in a recent interview with CNBC, Jamie Dimon, CEO of JP Morgan Chase, voiced a similar view of the world and its urgent implications:

“We have a longer-term problem now, which is that the world is not producing enough oil and gas to reduce coal, make the transition [to green energy], and produce security for people.”

“This should be treated almost as a matter of war at this point, nothing short of that.”

In search of ways to capitalize on this macro view of higher energy prices, today I’d like to discuss a company in the oil and gas sector called Tidewater (NYSE: TDW), one of the world’s leading offshore support vessel (“OSV”) operators. Tidewater checks many of the boxes for an attractive investment:

Trading at a significant discount (>60%) to underlying asset value

Potential free cash flow yield of over 20% in 2-3 years

Largest player in an industry entering the early stages of a multi-year bull market cycle

Zero net debt and virtually no risk of default

Strong management team with a track record of operating efficiency and M&A success

Here is a quick financial summary for the company:

An initial look at the share price history over the past couple of years may prompt the question – why is the author pitching a stock that has already fully recovered its pre-COVID high? Hasn’t the train already left the station?

My response would be a resounding no. An observer raising such a question would be making the grave mistake of merely looking at the stock price for information regarding intrinsic value. Although clearly it would have been more attractive to invest at the lower valuations in years past, I believe Tidewater is still significantly undervalued and provides a compelling opportunity to deliver a 2-3x return over a 2 to 3 year investment horizon.

Preface: This post is a high-level discussion and is not meant to be a complete analysis of the underlying thesis. I encourage interested readers to conduct further research as there is plenty of discourse and helpful information in the public domain.

Company Overview

Founded in 1955, Tidewater is a publicly-traded OSV company that provides offshore marine support and transportation services to the global offshore energy industry. The company currently owns and operates a diversified fleet of 195 vessels of various specifications, enabling it to provide services that include anything from carrying large equipment for the construction of oil rigs and wind farms to transporting supplies and crewmen to the offshore platforms.

The OSV business is fairly simple. Tidewater owns a variety of vessels – platform supply vessels (PSVs), anchor handling tug supply vessels (AHTS), crew boats (FSVs) – that differ in price and service capabilities and are spread out across the world in virtually all major offshore oil producing regions. The company operates in 5 distinct business segments, divided geographically: the Americas, Europe/Mediterranean, Asia Pacific, West Africa and the Middle East.

The primary customers are offshore oil and gas operators (primarily large international and state-owned oil companies) and increasingly offshore wind farms. Vessel services are typically contracted based on a fixed base rate (referred to as “vessel day rates”) and contract durations vary greatly depending on the scope of the project. Short-term contracts range anywhere from 1 day to 3 months while long-term contracts range between 3 months and several years. As a result, revenues are recognized daily throughout the contract period.

From a revenue perspective, an OSV operator is focused on optimizing three key elements: fleet size, vessel utilization and vessel day rates. The primary goal is to have every vessel contracted and active for as many days in the year as possible and at the highest day rates. Occasionally vessels do need to be put out of service for repairs and maintenance (“R&M”), upgrades, and required inspections (known as “dry docking”; twice every 5-year period).

On the expense side of things, there are five primary operating costs: crew/personnel, R&M, insurance, fuel, lube oil and supplies, and other operating costs, which include brokers’ commissions, training costs, port fees, etc. Out of all of these costs, crew and R&M costs are generally the largest components.

The cost structure in the OSV business is largely fixed in nature – once you have the boats staffed and maintained, the only remaining variable costs of note are really the brokers’ commissions and fuel and supplies. This business model thus allows for significant operating leverage, which is a very important factor in an environment of rapidly improving fundamentals and increasing prices.

OSV Industry from a Capital Cycle Perspective

The OSV industry is a deeply cyclical industry that follows the oil and gas market’s boom and bust cycle. Bob Robotti, a major Tidewater shareholder and successful value investor with experience in the OSV space for over 40 years, describes the demand for OSVs as a “first derivative of the price of oil”. This connection is intuitive: as oil and gas prices fluctuate, oil and gas companies adjust their CapEx and spending on offshore oil and gas projects, which in turn affects the demand for OSV services.

Given the cyclical nature of the industry, it helps to approach the thesis from the context of the capital cycle framework.

When oil and gas prices are high and future expectations are favorable, strong OSV demand leads banks and equity investors to shower OSV companies with easy capital. Companies load up balance sheets with debt to finance new boats and fleet upgrades while new players enter the market in hopes of getting a slice of the growing pie.

As the cycle progresses, the growth in supply and competition starts to outpace the growth in demand for OSVs, thus reducing profitability and returns for all players involved. When oil and gas prices decline, offshore oil and gas companies curb spending, and demand for OSVs plummet, leading investors to turn pessimistic and withdraw capital from the industry. Players are then stuck with a supply overhang, limited profitability, and inefficient operators go out of business as cash flow becomes insufficient to meet debt burdens. After a certain period of industry pain, oil prices begin to recover again and the supply side improves relative to demand, allowing the remaining survivors to regain their footing and earn above-average returns.

The Last Bull Market Cycle

A similar story has played out in the industry over the past couple of decades. The 2000s commodities boom was very favorable for the OSV industry – oil prices increased from a low of $20 at the end of 2001 to a high of $140 during the peak of the GFC in mid 2008. Although the price of oil briefly cratered to $42 by early 2009, it quickly recovered to the $100 range and stayed there until mid-2014.

The protracted boom in oil fueled significant growth for the OSV industry. Flush with cheap capital and favorable fundamentals, companies leveraged their balance sheets to upgrade their fleets in hopes of capturing greater market share. New competitors entered the market and supply grew aggressively throughout the period. From July 2008 to November 2014, the global population of OSVs grew from 2,033 vessels to 3,233 vessels, an increase of 59%. OSV supply outpaced demand as the OSV to oil rigs ratio increased from 3.37 to 4.49 OSVs for every oil rig.

In mid-2014, the cycle finally turned – oil prices began a steady decline from a high of $105 to a low of $33 by early 2016, a decrease of ~70%. Investment spending for offshore oil and gas projects collapsed and with it the demand for OSVs. The OSV industry entered into a painful bear market that forced many major players into bankruptcy, Tidewater included, as oversupply plagued the market and demand remained weak.

Although offshore oil and gas activity began to slowly recover in the 2017 to 2019 period, the COVID pandemic in 2020 quickly thrust the industry back into survival mode for the following 2 years. More players exited the business and significant supply was removed from the market. The recovery in oil prices throughout 2021 and 2022 has finally started to improve demand fundamentals for the industry, pushing the cycle into the most favorable period for investors: when improving supply side economics causes returns to rise above the cost of capital and share price outperforms.

Tidewater Performance during the Last Cycle

As one of the largest and most experienced players in the industry, Tidewater benefited greatly from the favorable macro backdrop of the 2000s. The company generated strong and consistent cash flow, returns on equity averaged in the low-to-mid teens range, and profit margins were relatively stable. Demand growth for OSVs outpaced supply growth and returns were above the cost of capital.

Not surprisingly, equity shareholders were handsomely rewarded: from the beginning of 2000 to the beginning of 2008, Tidewater’s share price averaged an annual return of ~9%; including dividends, the total return was ~10-12%, in line with the average return on equity. This compared favorably to the average annual total return from the S&P 500 of 1.7% throughout this 8-year period.

Following the GFC period, the industry started to show signs of weakness. With the temporary collapse in oil prices and increased uncertainty for global markets, spending for offshore oil moderated leading to a decrease in demand for OSVs. Overall demand levels took roughly 2.5 years (early 2011) to recover to pre-GFC levels.

The timing could not have been worse for Tidewater. Beginning in the early 2000s, Tidewater embarked on a multi-year campaign to completely upgrade its fleet. For context on the scale of the program, over a 15-year period ending mid-2014, Tidewater invested ~$5.2 billion in CapEx, which included spending for both new-builds and younger vessels. The average economic age of the fleet declined from a high of ~20 years in early 2006 to a low of ~5.5 years by mid-2010, reflecting the magnitude of the transformation.

This need for constant reinvestment is naturally very capital intensive. To fund the $5.2 billion in CapEx, as well as maintain its dividend and share buyback program ($1.3 billion), Tidewater had to borrow debt as cash flow from operations (“CFO”) only totaled $3.9 billion. As a result, when oil prices collapsed in 2014 and 2015, Tidewater was caught flat-footed. Despite owning one of the youngest and most competitive fleets in the world, the company was stuck with an overleveraged balance sheet and plunging profitability. Performance declined significantly over the ensuing 2 years and by mid-2017, Tidewater was forced to file for Chapter 11 bankruptcy and restructure its debt. Existing equity shareholders were wiped out and the debtholders became the new owners in the company.

A New and Stronger Tidewater

Tidewater emerged from Chapter 11 bankruptcy in a much stronger position compared to its competitors. The company started anew with zero net debt and one of the youngest and highest quality fleets in the world; meanwhile, the rest of the competition was weighed down by significant debt burdens and aging fleets. Tidewater gained significant financial wherewithal to weather the rest of the storm and the ability to capitalize on M&A opportunities once the cycle turned.

As a result of the bankruptcy, Tidewater had to apply fresh start accounting to the new entity – which essentially erases prior accounting records and establishes a new basis of accounting for all assets and liabilities based on the new capital structure. Assets on the balance sheet were written down by over 70%, despite the vessels being largely the same as they were pre-bankruptcy. This created a very large gap between accounting value and replacement value of assets – a gap that exists to this very day and plays an important role in the investment thesis.

In July 2018, a year after the bankruptcy, Tidewater merged with Gulfmark Offshore, another major player that had also emerged from Chapter 11 bankruptcy in 2017, and became the world’s largest OSV operator. This transaction showed an important strategic, albeit temporary, advantage that Tidewater had over others in the industry – the ability to consolidate smaller competitors and grow market share through acquisitions.

Tidewater experienced great success integrating Gulfmark. Initially, management expected to realize G&A synergies of ~$45 million by reducing combined G&A of $145 million to ~$100 million. However, by the end of 2019, they managed to beat their own expectations and reduced the G&A further to a run-rate of $87 million a year, showing management’s focus on operating efficiency and success with M&A.

Similar to others in the industry, Tidewater had a difficult period throughout COVID. Although earnings were poor during this period, the company had very minimal risk of default due to its net debt position and even managed to stay cash flow positive in both 2020 and 2021. Tidewater leveraged the downturn by upgrading the quality of its fleet and optimizing the underlying cost structure to best prepare for the eventual recovery.

So where is Tidewater now? Earlier this year, the company made another strategic acquisition, Swire Pacific Offshore, which added 50 vessels to the fleet. This addition strengthened its presence in several key markets, and cemented its position as the leading OSV operator in the world. With a clean balance sheet, an experienced and focused management team, and a world-class OSV fleet, Tidewater is now uniquely positioned to take advantage of the growing fundamentals in offshore oil and gas and the OSV industry.

Valuation

Net Asset Value

In terms of valuation, let’s first start with the assets. The single largest asset is the underlying value of the fleet. As of Q3 2022, overall net PP&E for Tidewater was ~$816 million. However, as mentioned earlier, book value does not accurately reflect the underlying value of Tidewater’s assets since they were marked down by over 70% post Chapter 11 bankruptcy.

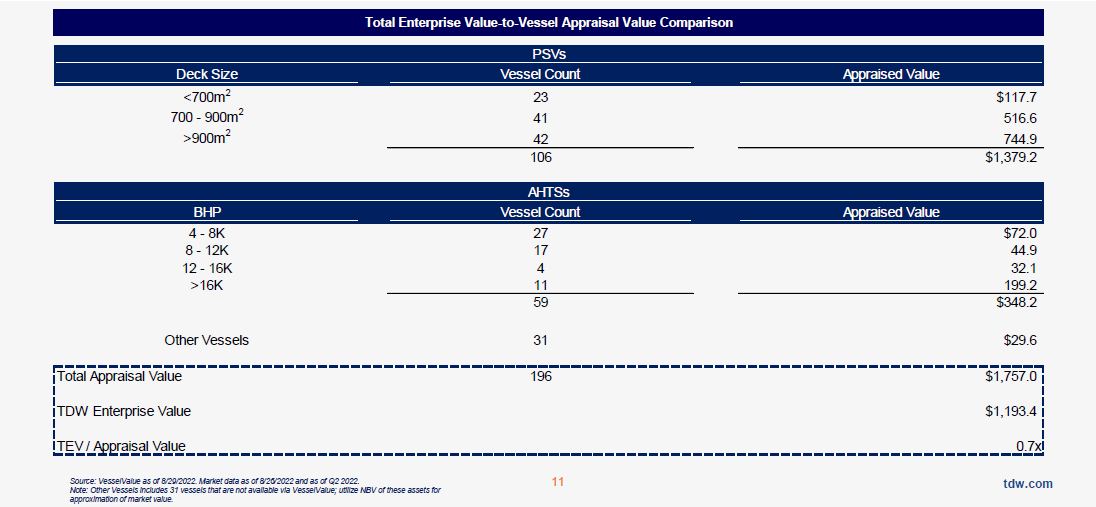

An alternative figure that may give us an idea for asset value is fleet appraisal value. In the company’s most recent September 2022 investor presentation, Tidewater provides a table comparing the company’s trading value and the company’s fleet appraisal value:

Total fleet appraisal value is estimated to be ~$1.76 billion. Since current EV hovers around ~$1.5 billion, the trading discount to appraisal value is in the range of 10-15%. At first glance, the size of this discount may seem rather unexciting. Why bother with a high risk investment in a heavily cyclical company if the discount to asset value is so narrow?

My view is the appraisal value is too conservative. To illustrate, let’s take a closer look at the top half of the table, which breaks down Tidewater’s fleet of platform supply vessels (“PSVs”). Tidewater currently owns 106 PSVs appraised at a total value of ~$1.4 billion, representing close to 80% of total fleet value. On a per vessel basis, the value averages out to ~$13 million per vessel: $5 million per vessel for the <700m2 category, $13 million for the 700-900m2 category, and $18 million for the >900m2 category.

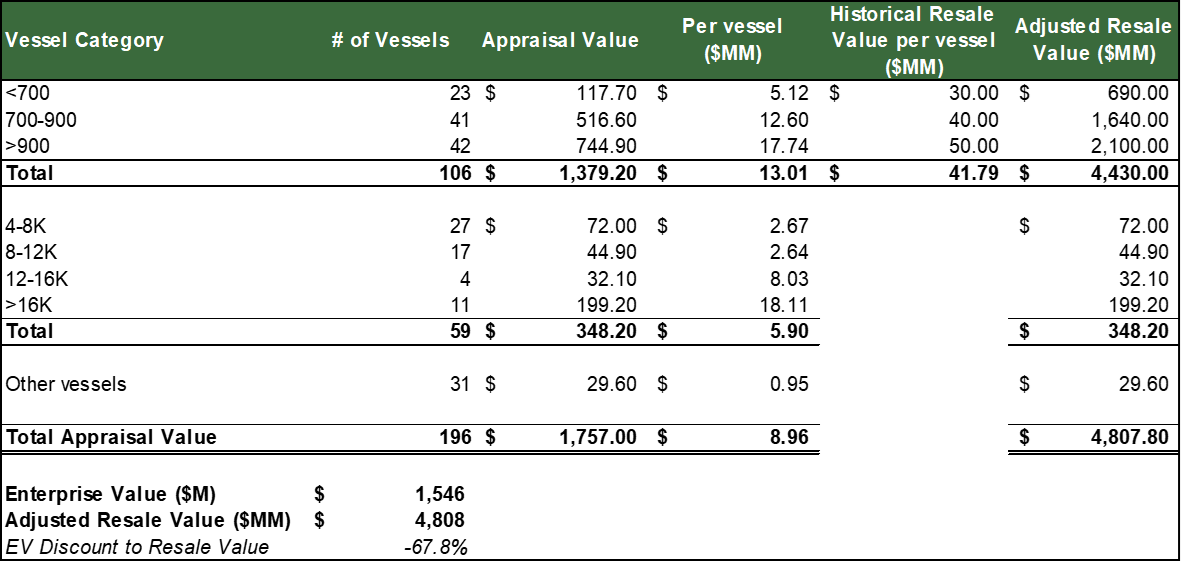

With these per vessel values in mind, let’s now take another approach and turn to the potential replacement value of the assets – i.e. what it would cost a competitor to replicate the assets necessary to operate the business. In the September 2019 Investor Presentation, Tidewater provided the following charts on PSV resale and newbuild values:

Between 2006 and 2014, average resale values for PSVs averaged around $30 million for the smaller category vessels (700 m2 deck), $40 million for the medium-sized vessels (800 m2 deck), and ~$50-55 million for the largest category vessels (1,000 m2 deck). These resale values were realized during the past bull cycle when vessel day rates hovered closer to $30,000 per day for the largest category PSVs and ~$20,000 per day for the smaller category vessels. As the industry recovers, it is reasonable for us to assume that resale and newbuild costs would increase and may rise above the levels that dominated the prior cycle due to inflation and supply chain challenges.

By simply using these resale values, the valuation gap between Tidewater’s current trading value and fleet replacement value suddenly becomes a lot more compelling:

It’s important to stress that when it comes to the OSV business, vessel quality matters. Higher spec and younger vessels tend to have much higher utilization and are also able to command much higher average day rates. Since emerging from bankruptcy in 2017, Tidewater has put a lot of effort into rationalizing its fleet size and optimizing quality towards higher spec vessels. In addition to disposing of older and lower spec vessels, Tidewater has also had the advantage of being able to maintain its fleet in good condition while industry peers have had to defer maintenance and fleet investment. This advantage in quality will enable Tidewater to dramatically increase day rates and drive profitability in the coming bull cycle.

Earnings Power Value

The earnings prospects for Tidewater are equally attractive. Q2 2022 marked a major inflection point for the market. The most important indicator for strength – vessel day rates – increased by nearly $1,900 per day during the quarter, eclipsing well beyond the $1,500 per day annual increase that is usually expected in past up-cycle periods. Average day rates increased a further $1,100 per day in Q3 2022, bringing 2022 YTD day rate growth to $3,000 per day. These increases in average day rates clearly show the tightness and momentum present in the market and bodes very favorably for demand growth in 2023 and beyond.

The growth in day rates have important implications for the growth in revenue and earnings. Given the high operating leverage, incremental increases in revenues from higher day rates and utilization are expected to flow right through to the bottom line, thus boosting profitability and potential returns to equity shareholders. According to Tidewater management, here’s what EBITDA could look like if utilization recovered to 90% and average day rates simply returned to peak levels achieved in 2014/2015:

Let’s set aside skepticism towards management estimates for a minute (which I don’t think are unreasonable). If these figures are realized, at a 91% FCF conversion rate, $666 million in EBITDA would translate to ~$600 million in FCF. Relative to current enterprise value of ~$1.5 billion, FCF yield would be close to 40% per year, an impressive figure for such a competitive and cyclical business. Imagine where EBITDA and free cash flow might be if average vessel day rates increase to $30k/day, not an unreasonable assumption given the company’s improved fleet mix and industry supply constraints. Tidewater would likely generate ~$1 billion in cash flow per year — not bad relative to current enterprise value.

When you compare the potential annual yields to those that could be achieved by investing in an S&P 500 index fund (maybe 5-6% over the next decade?), the decision seems rather obvious. However, as with other oil and gas investments, the stock price trajectory will have its fair share of volatility along the way. For those that can stomach the ups and downs, Tidewater will prove to be a highly profitable investment.

Disclosure

I am long TDW. As always, this is not investment advice. Please do your own DD before investing.